Before we dive into absorption costing and review how Beas Manufacturing works with it, let us outline some fundamental concepts of cost accounting that will play a key role in guiding us through this whole set of definitions and processes. Otherwise, it could be difficult to make sense of why certain processes must take place and their importance for enhancing a company’s decision-making capability by providing indispensable costing information.

Cost Accounting for Manufacturing Organisations

Cost, in its basic definition, is something everyone is familiarised with. After all, several decisions we take in our everyday lives depend on the many implications that costs have over variables we can and cannot control, like what is going to be our next car, to which school we will take our kids, where we will enjoy our next vacations, or in which city (or country) we are going to live.

In a business environment, however, costs represent a decisive factor in the companies strive for survival and growth. If a company has a non-competitive cost structure, it will ultimately become unfeasible to operate, as its profits will fall below acceptable levels, or its prices will soar above what the market is willing to pay for its products. Additionally, even when cost structures are competitive, incorrect costs appropriation might overburden some of the companies’ products while unburdening others, turning profitability analysis into a difficult and inaccurate task, and possibly leading to wrong business decisions. Therefore, understanding costs and being able to distribute them properly across the products is critical to success in a competitive environment.

If we think on retail or wholesale organisations, costs seem straightforward and are clearly identifiable in the products. Companies can easily know for how much they purchased their goods and pricing decisions are generally not complicated, as administrative expenses are either common to the entire company or related to product divisions and therefore easily linked to the goods. In this scenario, lowering purchasing prices and reducing structural costs have a direct impact on profitability, and understanding current profits doesn’t require much effort.

For manufacturing organisations, on the other hand, costs have a much higher degree of complexity, which arises especially from the fact that many manufacturing-related costs cannot be directly linked to a particular product. Nevertheless, instead of jumping straight into the tools we have for solving such problems and transforming complicated data into reliable and accurate costing information, let’s have a look at the components and definitions of cost for manufacturing companies.

There are three categories in which manufacturing costs are normally divided:

- Direct material: the costs of all direct materials consumed for manufacturing a product. If we think on a machined sandblasted metal piece, the direct material costs would come from how much metal we used to produce it, whereas other materials (such as sand wasted in the sandblasting process, drill bits, and end mills) whose measuring results impossible for that piece are treated as manufacturing overhead;

- Direct labour: all costs associated to the workforce physically and directly involved in the process of manufacturing a certain product. This accounts for machine operators and assemblers, but not for indirect labour, such as production supervisors, maintenance technicians and quality control operators;

- Manufacturing overhead: all other manufacturing costs which do not fall into the categories of direct material and direct labour are manufacturing overheads. This category includes costs of indirect materials (cleaning supplies, disposable safety equipment, disposable tools, fittings and fasteners, etc.), maintenance staff, quality control staff, equipment depreciation, utilities, factory rental, property taxes on the production facilities, production managers and supervisors, and many others. Manufacturing overheads do not include, however, administrative expenses not related to production—only indirect production costs can be considered as overheads.

Although it is fairly easy to measure direct materials and direct labour for manufacturing a product, understanding how much overhead costs each product should receive is always a complicated endeavour. For example, consider a company who produces liquid chemical products. Do all chemicals require the same reaction times on reactors and have the same viscosity? Not at all, and both higher reaction times and viscosity might represent a higher burden on maintenance and cleaning activities after production, as these products could wear the reactors faster and occasionally cause clogs which can be hard to clean. Besides, if the company constantly switches between different types of products using the same production resources, more cleaning and machine preparation times might be required than when producing multiple times the same product, which also increases manufacturing overheads significantly.

Using the traditional costing method, all manufacturing overheads would be summed and divided by the amount of a particular cost driver (which are the factors responsible for generating manufacturing costs), like the number of produced units, processed kilograms, or labour hours. Then, each and every product receives a share of manufacturing overheads based on how much of that same cost driver it contributed to increase. However, considering the existing variables in real production environments, should all products receive the same share of manufacturing overheads? If we produced 100 kilograms of a very difficult to process chemical, should it receive the same costs as 100 kilograms of an easily processable chemical? When the goal is to achieve a more accurate profitability analysis, the answer is no. And this leads to our next and fundamental question: how to make sure that each product receives a fair share of the correct manufacturing overheads?

For this question, the answer comes from one of the alternative methods to appropriate manufacturing overheads to products called absorption costing, which is precisely our next topic in this article. Using absorption costing, companies can base their costs appropriation on the costs related to direct or indirect manufacturing cost centres and on how much they affected production.

Introduction to Absorption Costing

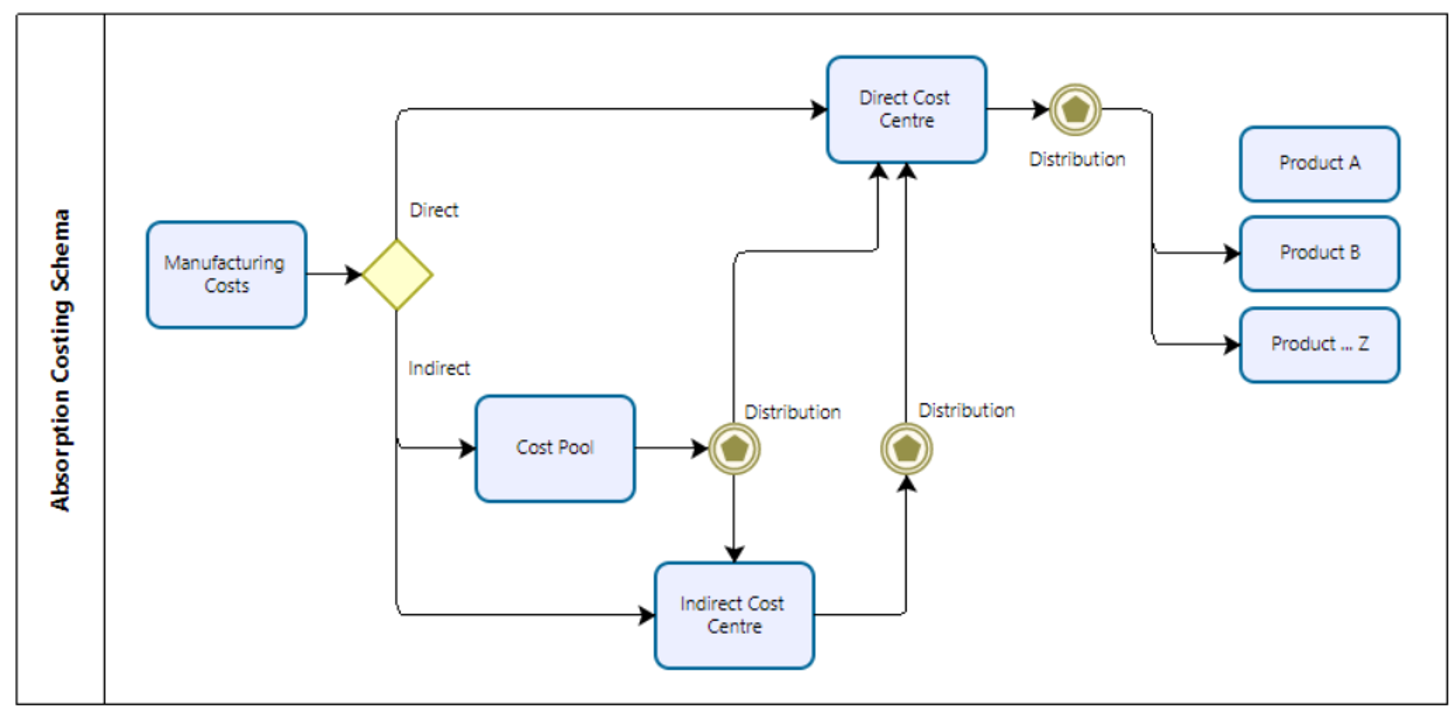

Absorption costing is a costing method targeted at distributing manufacturing overheads to the manufactured items and appropriating these costs into inventory, where they will remain until the company sells them. After selling, the products’ costs, now including manufacturing overheads distribution, will be recognised as COGS (Costs of Goods Sold) and affect the Profit & Losses financial statement. It is important to note that, apart from being an extremely useful tool for accurate per-product profits calculation, absorption costing is a mandatory requirement for publicly traded companies who need to follow GAAP and/or IFRS standards, and required by tax laws in the United States, Brazil, and many other countries.

When using absorption costing, the companies book all their manufacturing costs to cost centres, which can be direct or indirect. Direct cost centres represent manufacturing units directly related to production, like production equipment and work centres. Indirect cost centres, on the other hand, can represent either manufacturing units indirectly related to production (such as maintenance, production supervision, and quality control) or cost pools, which are intermediate cost centres that collect multiple costs before a further distribution into other direct or indirect cost centres. Afterwards, distribution rules will set the basis for sharing the costs contained in indirect cost centres across the direct cost centres, which will later be carried over into the products.

However, absorption costing can be an extremely complicated and time-consuming task without a powerful and integrated ERP to support it. Actually, several companies give up on absorption costing or treat it just like a burdensome obligation due to the simple fact that they lack the proper tools to calculate it properly. After all, for absorption costing to be successful, it needs to combine information coming from finance, production, maintenance, and many other departments, which can all have their own systems and require extensive manual work to match an immense amount of data in spreadsheets and input the results into the ERP. Nevertheless, when using Beas Manufacturing, you can be just a few clicks away from accomplishing a full absorption costing process, as it integrates manufacturing data to financial information coming from SAP Business One, automatically calculates the distributions of costs in between cost centres and products, and revaluate the goods based on their new calculated costs.

Now that we have reviewed the basics concepts of cost accounting and the implications of absorption costing for a manufacturing organisation, let’s take a look at how SAP Business One handles cost accounting and how Beas Manufacturing processes absorption costing, part of its Business Performance module.

SAP B1 and Beas Financial Integration

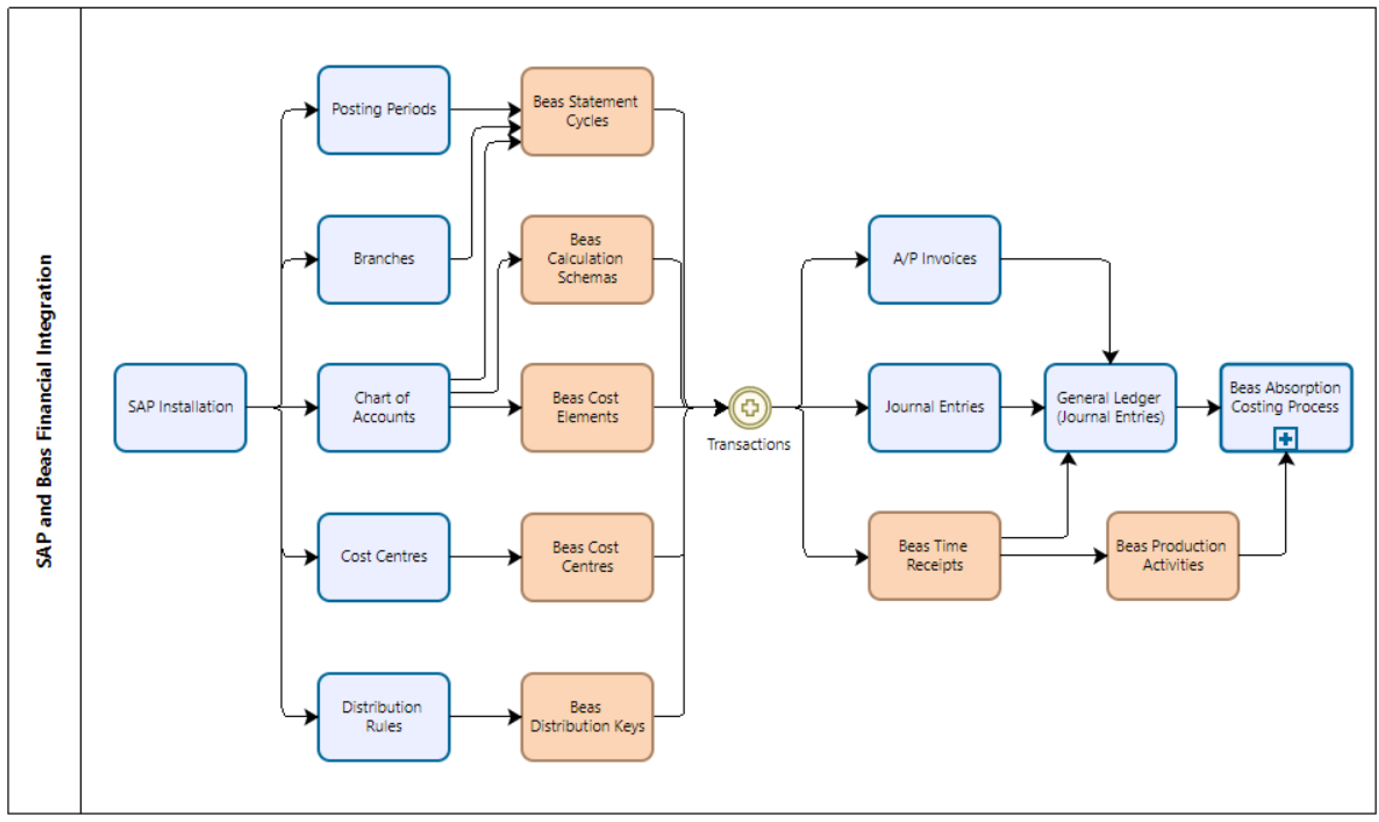

In an SAP Business One installation, the typical implementation process includes basic financial definitions such as posting periods, company branches (in the case of having multiple subsidiaries in the same database), chart of accounts, cost centres, and distribution rules (responsible for sharing values across multiple cost centres in certain transactions). Every time a user creates a transaction with inventory or financial implications, this transaction will trigger a journal entry containing manually selected accounts or automatically defined accounts based on accounting determinations, besides cost centres selected by the user or linked to the accounts.

For using absorption costing in Beas Manufacturing, extra definitions are required, like statement cycles mapped to the branches and posting periods, cost elements associated to the desired accounts from the chart of accounts, cost centres for direct and indirect manufacturing costs, and distribution keys reflecting SAP’s distribution rules. The linking in between manufactured items and direct cost centres happens through time receipts, which are the transactions generated to record processing times from factory workers and machines, and will later compose the production activities, or the list of manufactured goods to receive absorption costing appropriation.

Time receipts also trigger journal entries for labour and machine costs according to pre-defined resources and operators’ cost rates, in order to keep manufacturing costs as close as possible to the costs after absorption costing. These costs are automatically reverted as part of the absorption costing process (preventing double-costing on products, as they will receive labour, machine, and overhead costs from absorption costing) and, based on absorption costing results, output new recommended cost rates for production resources.

The flowchart below illustrates the integrations between SAP Business One and Beas Manufacturing for generating transactions and processing absorption costing.

Beas Business Performance-Absorption Costing

Beas Manufacturing, through its module Business Performance, provides an absorption costing functionality capable of distributing manufacturing costs (labour and overheads) to the produced goods, including distributions from cost pools and indirect cost centres to direct cost centres, detailed control of open absorption costing values for unfinished production orders at the month’s end, and redirection of subassemblies’ appropriations to the products who consumed then. Absorption costing affects inventory values, expenses, and costs of goods sold (if the products to revaluate were already sold during the month) by moving production-related expenses into inventory. This means that, after executing absorption costing, the company’s profits will be higher unless it has sold all its produced inventory, as manufacturing costs are only recognised as expenses in the form of COGS.

As mentioned before, absorption costing is a mandatory requirement for publicly traded companies who need to follow GAAP and/or IFRS standards, and required by tax laws in the United States, Brazil, and many other countries. By having Beas Manufacturing in place, your company can transform the burden of fulfilling tax requirements or complying to financial standards into a powerful and automated analytical tool for understanding costs and profits, requiring a fraction of the effort normally required by the traditional manual calculation methods.

Comments

0 comments

Please sign in to leave a comment.